Equities or bonds? Navigating the uncertainty

What our monetary tools are suggesting for March

Background

Each month we apply our Austrian economics monetary framework to several asset allocation questions. The emphasis is to take Austrian theory and apply it as rigorously as we can to real-world decision-making.

As with our previous Monthly Stocks/Bonds Timer posts, subscribers are encouraged to revisit our Framework post which outlines the methodology we apply in using the Liquidity cycle - the cycle of money supply growth versus money demand growth - for timing the changes in relative weights between stocks and bonds in a mixed portfolio.

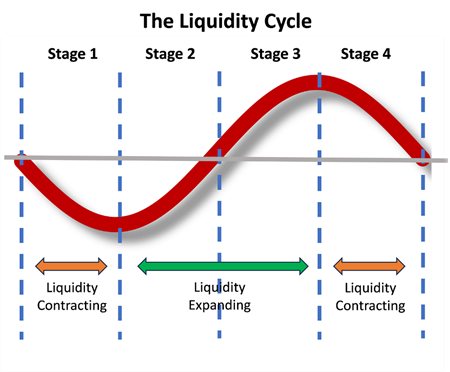

In this framework relative stock and bond weightings are determined by the economy’s stage in the cycle as displayed schematically below.

The relative weightings table below reflects the risk tolerance in each of the stages above. The weightings are relative to a standard 60/40 stock bond portfolio.

Below, we update our model stock/bond weightings for:

The US

Eurozone

Japan

UK

Australia

Canada

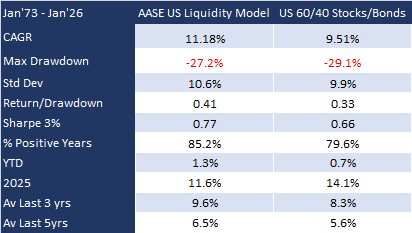

For the US, for example, the application of our liquidity-based timing of allocation shifts between stocks and bonds has delivered a useful performance edge over the standard, passive, 60/40 portfolio. Here are the notional historical results:

Below, we discuss the application of the approach to the listed countries, beginning with the US.